Banking up The Wrong Tree: Have the Climate Protests Against Financial Institutions Missed their Mark?

Extinction Rebellion protestors in New York City’s financial district. Photo by Felton Davis.

By Noah Yosif

Climate activism has historically focused on private industry. Since the early 1990s, most climate-driven campaigns have focused on individual companies, encouraging them to adopt corrective measures and environmentally-conscious business practices. Recently, this focus has changed. Activists have now found alternative targets in the financial services sector, particularly in global banks with investments in the fossil fuel industry.[1]

Environmental leaders now demand these financial institutions require environmentally-conscious business practices from their clients. To date, however, the financial services sector has been largely unresponsive. Recent studies show that many of the world’s largest banks have increased their support for companies across the fossil fuel lifecycle, devoted few resources toward sustainable activities, and retained poor internal controls to moderate their relationships with the fossil fuel industry.[2][3][4]

The divergence between activists’ demands and financiers’ decisions begs two questions:

Are financial institutions capable of exercising discretion against industries that damage the environment?

If not, where should climate activists focus their attention instead?

This article answers these questions by evaluating the fundamental assumption of climate activism toward the financial services sector: that banks can adequately circumscribe the behaviors of the fossil fuel industry. If they can, climate activists should continue to focus on pushing for financial institutions as enablers of the fossil fuel industry. If they cannot change corporate behavior, then the assumption is proved faulty, and climate activists should change the focus of their efforts.

The analysis below finds this assumption to be faulty in two steps. First, using the principle of social neutrality, a fundamental principle in banking, this article explains why climate activism has not yet led to significant divestment in fossil fuels from banks. Then, with data from several watchdog organizations, it illustrates how financial regulatory authorities, rather than private banks themselves, may prove more influential over private sector behavior. The data shows that in countries with stronger climate policies, from controls on emissions to incentives for renewable energies, banks generally maintain a smaller portfolio in fossil fuels and other environmentally-damaging industries. Lastly, this analysis also suggests that central bankers, rather than private financiers, may be better worth the activists’ attention.

Climate Protests & Bank Behavior

Transnational banks have become a new target for climate activists. Industry groups like BankTrack, Reclaim Finance, and BankFWD, have publicized the ties between fossil fuel producers and the financial services sector.[5] The Sunrise Movement and the School Strike for Climate Change have organized demonstrations outside banks’ offices to draw attention to their contentious investments.[6][7] From both within and outside the industry, activists are drawing public and regulatory attention to banks’ environmentally-damaging clients and practices.

The climate activists’ demands broadly challenge the banking principle of social neutrality, a concept that allows banks to serve any legal business that generates investment returns. Historically, financial institutions have relied on this principle to justify controversial, but legal, investments, such as those in firearms manufacturers and private prisons.[8][9][10] On occasion, however, banks depart from this principle, particularly in cases where one of the three conditions are met:

Unambiguous optics (e.g. banks refusing diamond dealers unable to verify their products are not “blood diamonds”[11]);

Strict regulation (e.g. banks denying services to sanctioned individuals accused of human rights abuses[12]); or

Reputational risks that may affect their balance sheet.[13]

By drawing public and regulatory attention to questionable investments, climate activism appears to pressure banks on each of these three points. To date, however, this has not led to significant divestment from fossil fuels or other environmentally-damaging industries. If these three conditions have led banks to sever ties with other problematic clients before, why wouldn’t they do the same for fossil fuels? The unfortunate reason is that none of the three conditions are met to a sufficient degree to change bank behavior.

First, fossil fuel companies are much more ingratiated than the firearms industry or private prisons. They retain significant political power, employ thousands, and provide a source of energy on which economies still depend. Though public opinion has begun to turn against the industry, it has not fallen so far as to threaten investment returns. For banks, the optics of their investments are not sufficiently unambiguous.

Second, differences in international climate policies have created a lenient regulatory environment. Financial institutions in less-regulated countries can more easily serve fossil fuel companies than those in countries with mandatory disclosure laws or financial penalties for environmental damages. With discrepancies between countries, regulations are not yet strict enough to elicit behavior changes from global banks.

Third, the number of global financial institutions makes universal behavior change difficult. There are over 240 multinational financial institutions with at least $100 billion in total assets, plenty for the needs of any of the top twenty fossil fuel producers responsible for one-third of all global carbon emissions.[14][15][16] Each of these large banks must consider their own unique reputational risks, financial exposures, and regulatory concerns. Where one may decide to divest from fossil fuels, another might be willing to take its place.

This means that climate activism toward financial institutions will not prove effective on its own. The assumption that financial services can adequately circumscribe the behavior of polluting industries is not sound. At present, financial institutions are not capable of exercising discretion against fossil fuel producers, because the fossil fuel industry has not yet met any of the conditions that would incentivize banks to disregard the principles of social neutrality and divest from the fossil fuels.

Climate Regulation & Bank Behavior

Climate policy, rather than private financial institutions, may prove a better target for climate activists. Climate policy, defined here as a given government’s set of regulations against environmentally-damaging activities, could change banks’ views of offending industries. By clarifying the optics of fossil fuel investments, promoting consistency between international regulations, and driving up the reputational risks, policymakers can create an environment where banks may no longer find cover under the principle of social neutrality.

Data from industry watchdogs suggests this process is already under way. In countries with strong climate policies, banks appear to have stronger internal controls governing their relationships with the fossil fuel industry, while those from countries with weak climate policies have poorer controls. Metrics from BankTrack and Germanwatch illustrate this association.[17][18] BankTrack is a reputed financial services watchdog which publishes annual evaluations of banks’ internal controls (based on public statements, disclosures, commitments, and other metrics) pertaining to their service of the fossil fuel industry. Germanwatch is a nonprofit organization specializing in environmental policy research, best known for producing its annual Climate Change Performance Index which evaluates greenhouse gas emissions, renewable energy adaptation, energy consumption, and climate policy. For either metric, a higher score is considered more desirable. In countries with climate policies scoring above the benchmark of 70 in the Germanwatch climate policy scale, banks score an average of 46.5 in BankTrack’s institutional policy score. Banks from countries with climate policies scoring below 70 have a BankTrack average of just 23 (See Figure 1).

Figure 1: Average Institutional Fossil Fuels Finance Policy Scores to Countries’ Climate Policy Scores

Source: Author’s analysis using data from BankTrack (2020), Germanwatch (2019), and S&P Global Market Intelligence (2021)[19]

Higher Germanwatch climate policy scores are also associated with declining investments in the fossil fuel industry. Additional data from the Rainforest Action Network (RAN) provides the total change in investment between 2016 and 2019 for major multilateral banks by country.[20] Countries that saw a decrease in their institutions’ fossil fuel holdings posted an average climate policy score of 67.3, compared to 49.3 among countries that saw a net increase in their institutions’ fossil fuel holdings. Financial institutions in the low-ranking countries, such as the United States and Japan, greatly increased their investments in fossil fuels over the period. This trend suggests that climate policies not only encourage banks to improve their internal controls toward fossil fuel companies, but also to divest from them.

Figure 2: Change in Institutional Fossil Fuels Financing to Countries’ Climate Policy Scores

Source: Author’s analysis using data from Rainforest Action Network (2020), Germanwatch (2019), and S&P Global Market Intelligence (2021)[21]

Additionally, strong climate policies appear to be associated with greater investment in sustainable activities, and less investment in fossil fuels. In light of increasing scrutiny over their fossil fuels investments, many banks have announced sustainability commitments.[22] These commitments vary by country and their individual climate policies. Data from the World Resources Institute, which tracks banks’ financing in both fossil fuels and green initiatives, implies that banks from countries with strong climate policy scores generally have greater sustainability commitments and less investment in fossil fuels.[23] For banks from countries with weak climate policies, the opposite appears true (see Figure 2).

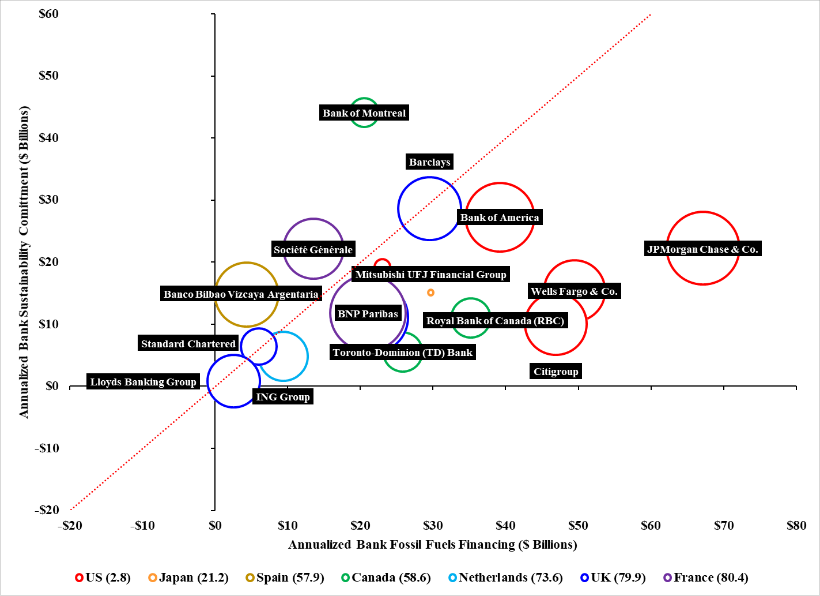

Figure 3: Ratio of Institutional Investments within Fossil Fuels to Sustainable Activities

Not all banks labeled. Source: Author’s analysis using data from World Resources Institute (2019), Germanwatch (2019), and S&P Global Market Intelligence (2021)[24]

Comparisons of these data from watchdog groups suggest that bank behavior varies according to a country’s climate policy, and banks are not inherently inclined to change their behavior absent of such a policy. Despite pledging large sums of capital toward sustainable activities, most banks devoted a higher share of finances to fossil fuels. This is shown in Figure 3 by the banks’ positions below the red line indicating an equitable allocation of finances between both activities. The banks with the most egregious discrepancies are located in the United States, Canada, and Japan – countries with relatively weak climate policies as per Figures 1 and 2. This analysis suggests that if these countries had stronger climate policies, these banks would likely have fewer investments in fossil fuels.

Given the small sample size of countries considered here, the possibility of omitted variables, and the descriptive nature of this analysis, this study cannot claim to have established the exact relationship between climate policy and bank behavior. Further testing is needed to establish statistical significance and infer causation. This comparison of watchdog data, however, suggests a valuable hypothesis for climate activists, especially as they expand their focus from private industry. Through sharper optics, greater regulation, and clearer reputational risks, stronger climate policies appear to change bank behavior where it would not otherwise have changed, pushing more banks to reevaluate their services to the fossil fuel industry and depart from the principle of social neutrality.

Central Banks: A More Receptive Ear?

If climate policy appears to be a more effective campaign target than individual companies, which policymakers should the climate activists target? On the specific issue of fossil fuel finance, central banks may prove their best focus. As the primary regulatory authority for all private financial institutions in a given country, central banks constitute a unique opportunity for activists to change the dynamics which enable fossil fuel financing.

Three features of central banks make them worth activists’ attention. First, central bankers have an expertise on the banking system that many other policymakers lack. Second, they are a principal architect of national financial policies, often working in tandem with treasury departments and other government agencies. Third, they have a wide purview. The 240 largest financial institutions are accountable to just 15 central bank authorities (if the 11 central banks of the Eurozone mandate are considered together).[25] Central bankers may be the most powerful authority in getting financial institutions to reevaluate the social neutrality principle along the green lines.

Indeed, many central banks have already begun to include climate-related priorities in their oversight of private financial institutions (see Figure 4). Some measures, such as incorporating climate risks into stress tests and mandating disclosure of certain climate-related assets, have improved transparency within the financial services sector. These measures enable regulators to examine bank-specific exposures to the fossil fuel industry.[26] Other actions, such as enacting subsidies for “green” investments in renewable energy sources and taxes on “brown” investments in non-renewable energy sources, have created meaningful incentives for banks to modify their behavior while maintaining a healthy profit. Some central banks have supplemented these bank-specific measures with climate-conscious monetary policies toward the economy at-large, such as issuing green bonds and promoting investment within sustainable activities.[27] Altogether, central banks not only possess the regulatory authority necessary to change bank behavior, but they also act as the unique monetary policy authorities that could spur systemic, climate-conscious changes to the economy at-large.

Many of these policies are still in their infancy. They will take time to affect the global financial services sector. In the meantime, this is also an opportunity for activists. The recent uptick in global climate activism has accelerated the pace by which central banks include climate-related priorities within their regulatory and policy-making activities. Further activism may prove essential to keeping momentum behind these new central bank policies. Global networks of activists can pressure central banks to match the policies of their peer regulators in other countries, helping to avoid the regulatory discrepancies that banks and fossil fuel producers exploit. Reduced discrepancies would prompt the private banks to view fossil fuel investments as bearing significant reputational risks, eventually leading to divestment. These efforts would be important both to central banks just getting started with climate policies (such as the U.S. Federal Reserve) and those with established, if imperfect, policies (such as Eurozone central banks).

Figure 4: Climate-Related Measures Enacted by Central Banks Around the World

Source: Author’s analysis using data from Official Monetary and Financial Institutions Forum, Mazars, Thompson Reuters (2020)[28]

Conclusion

Financial institutions may have proven unresponsive to the demands of climate activists, but their behavior is not inexplicable. Multinational banks themselves are not inclined to divest from fossil fuels due to the principle of social neutrality. While they have divested from controversial clients in the past due to unambiguous optics, strict regulation, and significant reputational risks, none of these conditions are sufficiently met to trigger divestment from the fossil fuel industry. Climate activism may have shifted public opinion, but it has yet to shift boardroom opinion to the degree necessary.

Climate policy, on the other hand, appears more effective in generating behavioral change among the banks. Financial institutions in countries that maintain robust climate policies tend to have stronger internal controls compared to their peers in less-regulated countries. They also tend to devote more resources toward sustainable activities and have lower financial exposures to the fossil fuel industry. This suggests that if climate policy was more consistent between nations, there would be less room in regulations for banks to exploit, and therefore a greater chance of change in banking behavior.

This hypothesis provides activists with a suggested blueprint for future efforts. Climate activists should persuade central banks, the most influential policymakers in the financial sector, to hone the optics of fossil fuel investments, improve regulations for such investments, and make the reputational risk of such investments clear to banks. Many central banks have already begun to implement some of these demands into their regulatory and policymaking activities, and climate activists can help maintain this momentum. Central banks, rather than private banks individually, may very well prove the most effective means for climate activists to achieve their goals.

Climate activists have a long road ahead to realizing a cleaner economy. A better understanding of the target will help them chart their path toward saving the planet more quickly and accurately.

About the Author:

Noah Yosif is an economist specializing in financial policy research pertaining to community banks and the federal banking system. He previously served in economic research roles at the U.S. Bureau of Labor Statistics, Department of the Treasury, and Federal Reserve Board. He is also a Master of Public Administration candidate at the Fels Institute of Government at the University of Pennsylvania, and holds a Masters in Applied Economics, as well as a Bachelors in Economics, from the George Washington University.

Endnotes

Lennox Yearwood Jr., and Bill McKibben, “Want to Do Something About Climate Change? Follow the Money,” The New York Times, January 11, 2020, https://www.nytimes.com/2020/01/11/opinion/climate-change-bank-investment.html. See also Zack Colman, “Climate Groups Turn Up the Heat on Big Banks, Insurers,” Politico, January 13, 2020. https://www.politico.com/news/2020/01/13/climate-groups-protest-098251.

Kalyeena Makortoff and Patrick Greenfield, “Study: Global Banks 'Failing Miserably' on Climate Crisis by Funneling Trillions into Fossil Fuels,” The Guardian, March 18, 2020, https://www.theguardian.com/environment/2020/mar/18/global-banks-climate-crisis-finance-fossil-fuels.

Valerie Volcovici, “World's Largest Banks Lagging in Sustainable Finance: Report,” Reuters, October 3, 2019, https://www.reuters.com/article/uk-climate-change-banks/worlds-largest-banks-lagging-in-sustainable-finance-report-idUKKBN1WI08O?edition-redirect=uk.

“Banks Warned That Deficient Fossil Fuel Policies Are Accelerating Climate Crisis,” BankTrack, December 12, 2019, https://www.banktrack.org/article/banks_warned_that_deficient_fossil_fuel_policies_are_accelerating_climate_crisis.

Saijel Kishan, “Fighting Climate Change by Shutting Down the Money Pipeline,” Bloomberg, February 4, 2021, https://www.bloomberg.com/news/articles/2021-02-04/climate-change-environmentalists-target-banks-to-cut-off-fossil-fuel-funding.

Ayse Gursoz, “Arrests Made at Chase Bank as Protests Escalate Against Bank's Funding Choices,” Rainforest Action Network, December 14, 2018, https://www.ran.org/press-releases/arrests-made-at-chase-bank-as-protests-escalate-against-banks-funding-choices/.

Alex Ruppenthal, “Protesters Disrupt Chase Shareholder Meeting Over Financing of Controversial Pipeline,” WTTW News, May 21, 2019, https://news.wttw.com/2019/05/21/protesters-disrupt-chase-shareholder-meeting-over-financing-controversial-pipeline.

This principle was recently outlined in a letter written by the Bank Policy Institute in response to proposed rule by the Office of the Comptroller of the Currency which would have required large financial institutions to provide “fair access” to clients from controversial industries, such as gun manufacturers or fossil fuels. The letter explains there is no need for such a requirement because financial institutions are inherently motivated to serve clients of all industry backgrounds, contingent on the financial tradeoffs associated with serving them, which are always evaluated by the bank. See Greg Baer, “Fair Access to Financial Services” (RIN 1557-AFO5, Bank Policy Institute, 2021). https://bpi.com/wp-content/uploads/2021/01/BPI-Fair-Access-to-Financial-Services-2021.01.04.pdf.

Anthony Noto, “After Swearing off Gun-Manufacturers, Bank of America Backs Remington,” New York Business Journal, May 7, 2018, https://www.bizjournals.com/triad/news/2018/05/07/bank-of-america-backs-remington.html.

Holding Wall Street Accountable, “The Banks Still Financing Private Prisons,” The Center for Popular Democracy, May 3, 2019, https://www.populardemocracy.org/blog/banks-still-financing-private-prisons.

Financial Action Task Force and Egmont Group of Financial Intelligence Units, “Money Laundering and Terrorist Financing Through Trade in Diamonds,” Financial Action Task Force, October 2013, http://www.fatf-gafi.org/media/fatf/documents/reports/ML-TF-through-trade-in-diamonds.pdf.

Carlo Edoardo Altamura, "Global Banks and Latin American Dictators, 1974–1982," Business History Review (2020): 1-32.

Hollie McKay, “US Banks and Financial Institutions Have Been Slowly Severing Ties With the Gun Industry,” Fox News, July 22, 2020, https://www.foxnews.com/us/us-banks-financial-institutions-severing-ties-gun-industry. See also Anna Hrushka, “Barclays Drops Private Prisons as More Banks Weigh Reputational Risks,” Banking Dive, Industry Dive, August 1, 2019, https://www.bankingdive.com/news/barclays-drops-private-prisons-as-more-banks-weigh-reputational-risks/560037/.

Total Assets by Institution and Country, V1, January 1, 2021, distributed by S&P Global Market Intelligence, accessed on January 15, 2021.

Matthew Taylor and Jonathan Watts, “Revealed: The 20 Firms Behind a Third of All Carbon Emissions,” The Guardian, October 9, 2019, https://www.theguardian.com/environment/2019/oct/09/revealed-20-firms-third-carbon-emissions.

Ibid.

“Banks and Fossil Fuel Financing,” Banks, Climate and Energy, BankTrack, October 30, 2020, https://www.banktrack.org/campaign/banks_and_fossil_fuel_financing#_.

Jan Burck et al., “The Climate Change Performance Index 2020: Results,” Germanwatch, December 19, 2019, https://germanwatch.org/en/17281.

“Banks and Fossil Fuel Financing.”; Burck et al.; Total Assets by Institution and Country.

Alison Kirsch et al., “Banking on Climate Change: Fossil Fuel Financing Report 2020,” Rainforest Action Network, March 18, 2020, https://www.ran.org/wp-content/uploads/2020/03/Banking_on_Climate_Change__2020_vF.pdf.

Ibid.; Burck et al.; Total Assets by Institution and Country.

Saijel Kishan, “Banks Tout Green Credentials Yet Cling to Fossil-Fuel Clients,” Bloomberg. October 3, 2019, https://www.bloomberg.com/news/articles/2019-10-03/banks-tout-green-credentials-yet-cling-to-fossil-fuel-clients.

Ariel Pinchot and Giulia Christianson, “How Are Banks Doing on Sustainable Finance Commitments? Not Good Enough,” World Resources Institute, October 11, 2019, https://www.wri.org/blog/2019/10/how-are-banks-doing-sustainable-finance-commitments-not-good-enough.

Ibid.; Burck et al.; Total Assets by Institution and Country.

Total Assets by Institution and Country.

Markus K. Brunnermeier and Jean-Pierre Landau, “Central Banks and Climate Change,” Centre for Economic Policy Research, VoxEU, January 15, 2020, https://voxeu.org/article/central-banks-and-climate-change.

Josh Ryan-Collins and Frank van Lerven, “Central Banks, Climate Change and the Transition to a Low Carbon Economy: A Policy Briefing,” New Economics Foundation, September 7, 2017, https://neweconomics.org/uploads/files/NEF_BRIEFING_CENTRAL-BANKS-CLIMATE_E.pdf.

Marc Jones and Dhara Ranasinghe, “Analysis: Central Banks Flexing Their Green Muscle for Climate Fight,” Reuters, October 28, 2020, https://www.reuters.com/article/uk-global-cbanks-green-analysis-idUKKBN27D1YK.